My Fee Structure

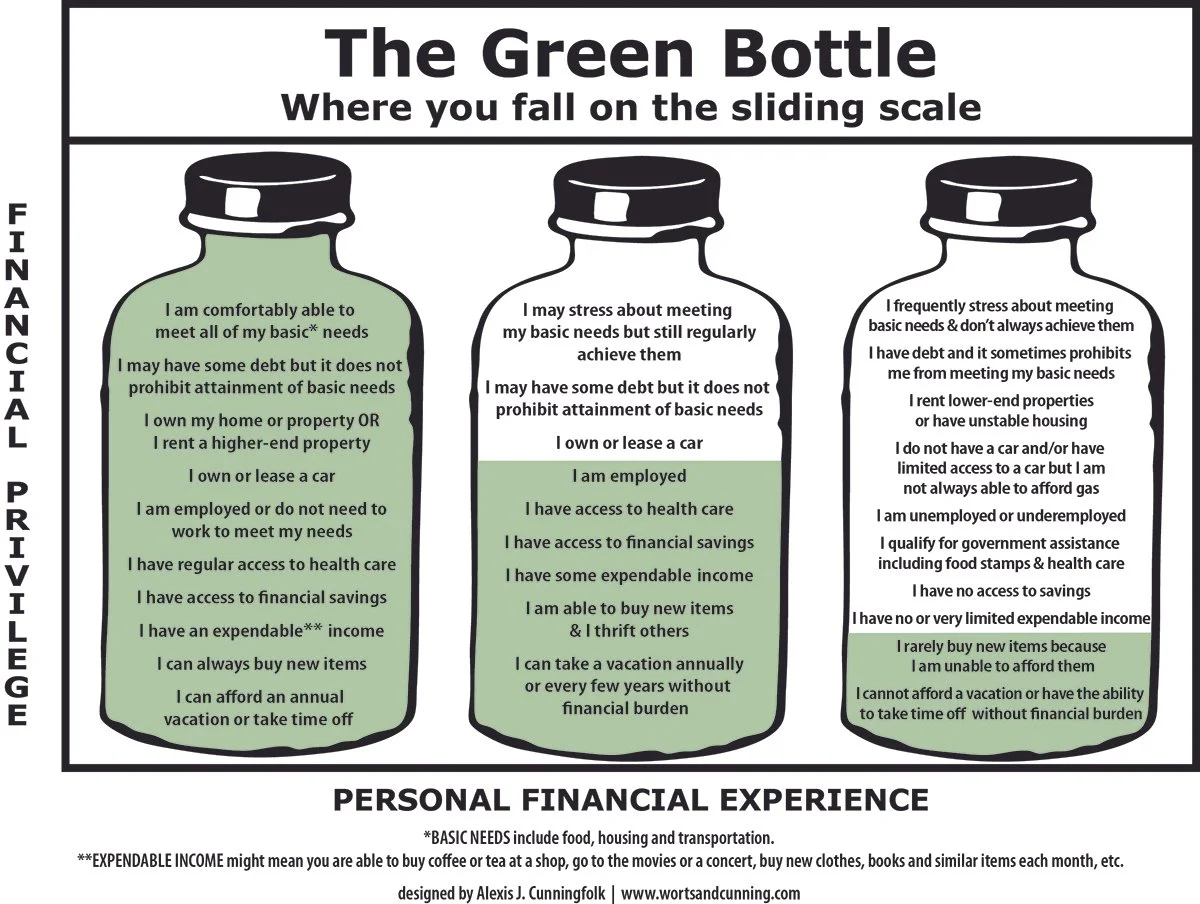

My sliding scale is based on Alexis J. Cunningfolk’s “green bottle” model for determining your particular financial circumstances. A lot of us may feel like we have fewer financial resources at our disposal but there is a difference between financial sacrifice and financial hardship.

If paying for therapy would be challenging but not detrimental, that may require financial sacrifice. Choosing therapy may mean having to reduce your other spending, or pull money from savings, etc. but if the financial cost doesn’t cause a long-term harmful impact on your life, it’s not a financial hardship. If, however, paying my standard therapy rate means you wouldn’t be able to pay for rent, buy food, or pay for transportation to get to work, then you’re dealing with financial hardship.

I do not ask for income verification; conversations about money are based on mutual respect, honesty, and accountability.

Why I Don’t Take Insurance

I don’t accept insurance for myriad reasons including, but not limited to, confidentiality and privacy issues, aversion to the medical model, the requirement of a formal “qualifying” diagnosis, etc. Insurance companies also like to dictate treatment based on their bottom lines and not what’s best for you.

Insurance companies are also notorious for low rates with delayed payments and retroactive claim denials, not to mention the ridiculous amount of time-consuming paperwork.

I recognize that not accepting insurance potentially creates an accessibility issue. Here are a couple of options to alleviate that:

You can pay for therapy using your FSA/HSA benefits.

I can provide a superbill that you can submit to your insurance company. Be aware that some insurance companies require a diagnosis on your superbill and there is no guarantee that your plan will reimburse your claim.